The interest calculated on credit cards can be troubling and confusing. Using a credit card wisely will save you money and keep you out of debt. Carrying balances over each month will lead to a larger balance, with you paying more than the original amount owed. This is due to the credit card interest calculated each month on the remaining balance. There could be other fees, such as over-the-limit fees, late payment fees, returned checks, membership fees, etc. Now your balance is much higher than the original amount the card was used for.

Annual Percentage Rates (APR):

Don’t be fooled by the word “Annual”, interest is not calculated yearly but done daily. This interest rate is applied each month on any outstanding balance on the card. Daily interest is calculated during the billing cycle; most cycles are 28-31 days. A percentage of interest is added to your balance at the end of each cycle. However, by paying off the balance each month it results in no interest being added on. Making the minimum payment or even a larger payment without paying off the balance will result in interest being added to your remaining balance.

How the APR is set:

Many variable interest rates are calculated by using an index, such as the U.S. Prime Rate, then the lender or bank adds a margin to achieve the desired APR. The U.S. Prime Rate index can change, which will affect the APR. Click here for the latest info on U.S. Prime Rates.

Get Started With a Free Debt Analysis

We make it easy on mobile or desktop. FREE with no obligations.

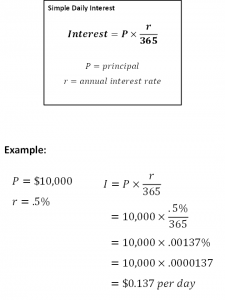

Formula:

The U.S. Prime Rate + the margin a bank charges = APR (Annual Percentage Rate)

How Interest is calculated:

Depending upon the card you have, some companies calculate a daily or monthly periodic interest rate.

Formula:

APR / 365 days = DPR (Daily Percentage Rate)

(DPR x Days in billing cycle) x Balance subjected to interest rate charges = Interest charged and applied

Or you can use this formula:

If an account has multiple APRs, each one has this calculation applied to it. Be careful because your Purchase APRs can differ from Cash Advance APRs. Read the fine print! We’ve always liked the saying “The large print giveth and the small print taketh away!” because it’s so true.

Different types of Interest Rates:

Fixed Rate –

Fixed rates are always the best option since the rate does not change without prior notification and time allowed for making adjustments. Your fixed rate cannot be changed without notice, and there are laws protecting the consumer from this. This may make you feel more comfortable, but credit card companies are tricky in how they inform you of these changes.

Some examples are:

- The fine print on your monthly statement indicating a rate change. It is written so small that you can easily miss it.

- Information pamphlets giving you an overview of various aspects of your card with a change to the interest rate listed among them.

- You use the email system for statements; the company may notify you of the change with this method. Check your junk mail often.

Don’t be misled that a fixed rate is the best deal; they can range from 2% to 30% or a much higher rate. You can benefit from a fixed rate since you will know each month what to expect when carrying over the balance.

Variable Interest Rate –

The variable rate can vary based upon the balance, payment history and other factors. This rate can change every month without prior notification. Your balance can skyrocket each month, and if you cannot make the minimum amount because of this, late fees are then added. This method puts many families in a bind that causes a hardship in paying down or paying off the remaining balance.

Introductory Interest Rate –

Credit card companies know how to draw customers in, and a low interest rate is one of their best tricks. They start you off at a low rate then slowly increase it. Another method of luring in consumers is the Introductory Interest Rate. These are extremely popular because of the low interest and balance transfer credit cards. Some start as low as 0% for a period of time, but reading the fine print is where the real details are. Interest may be compiled during the introductory period and any balance at the end will have that interest applied to the remaining amount.

While some offers are very appealing for introductory rates, the honeymoon is over at the end and rates go up. That minimum $20 monthly payment is suddenly $100, and you can’t afford that unexpected increase. As you struggle to figure out how to make this payment, the credit card company is applying interest and any additional fees to your balance.

Best advice on using these types of cards is pay off your balance completely before the introductory rate is over. You avoid paying high interest rates and have the option to cancel the card or not use it should the rate be drastically increased.

Be informed on the types of credit cards available and their interest rates to make the right decision on what card to choose. Read the fine print and understand that your APR might be variable and could change (go up) at any point in time. Keep track of everything!

Contact a certified credit counselor if you have any questions about credit card debt or just credit cards in general. Give us a call at 866-699-2227 or visit us online at www.advantageccs.org!