Have you ever wondered how credit cards came about? Who thought of the very first credit card and what were they used for back then? From personalized store credit in the 1800s to the never-ending card offers that pile up in your mailbox on a daily basis, credit cards have become an inescapable part of modern life.

As far back as the late 1800s, consumers and merchants exchanged goods through the concept of credit, using credit coins and charge plates as currency. It wasn’t until about half a century ago that plastic payments, as we know them today, became a way of life. I’d like to share with you a brief history about credit cards and the changes that have happened over the years.

Here’s How It All Got Started:

1885 – Merchants and certain financial institutions provided credit for agricultural and durable goods. These credit “cards” soon began to spread to other industries. Hotels and department stores offered their most valued customers paper credit cards. The cards were almost exclusively used at that one location. However, some local merchants would accept a competitors’ credit card. This is how it all got started.

1885 – Merchants and certain financial institutions provided credit for agricultural and durable goods. These credit “cards” soon began to spread to other industries. Hotels and department stores offered their most valued customers paper credit cards. The cards were almost exclusively used at that one location. However, some local merchants would accept a competitors’ credit card. This is how it all got started.

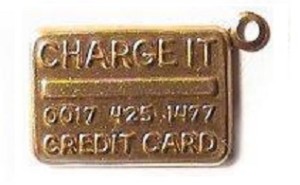

1946 – The first bank card, named “Charg-It,” was introduced by John Biggins. Biggins was a banker in Brooklyn, New York. When a customer used it for a purchase, the bill was forwarded to Biggins’ bank. The bank reimbursed the merchant and then obtained payment from the customer. There were a few catches though; purchases could only be made locally within the town, and cardholders had to have an account at the bank.

1946 – The first bank card, named “Charg-It,” was introduced by John Biggins. Biggins was a banker in Brooklyn, New York. When a customer used it for a purchase, the bill was forwarded to Biggins’ bank. The bank reimbursed the merchant and then obtained payment from the customer. There were a few catches though; purchases could only be made locally within the town, and cardholders had to have an account at the bank.

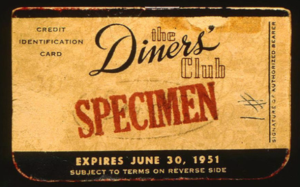

1949 – The Diners Club Card was the next step in credit cards and it was made out of cardboard. The Diners Club Card was used for travel and entertainment purposes, it claims the title of the first credit card in widespread use. A decade later, the card was replaced with plastic. Diners Club Card purchases were made on credit, but it was technically a charge card because the bill had to be paid in full at the end of the month.

1949 – The Diners Club Card was the next step in credit cards and it was made out of cardboard. The Diners Club Card was used for travel and entertainment purposes, it claims the title of the first credit card in widespread use. A decade later, the card was replaced with plastic. Diners Club Card purchases were made on credit, but it was technically a charge card because the bill had to be paid in full at the end of the month.

Get Started With a Free Debt Analysis

We make it easy on mobile or desktop. FREE with no obligations.

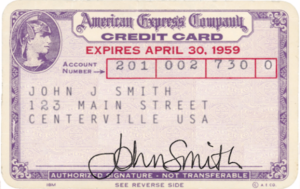

1958 – Bank of America and American Express saw the overwhelming success of the Diners Club Card and wanted to get in on the action. America Express created a purple charge card for travel and entertainment expenses. In 1959, AMEX introduced the first card made of plastic because previous cards were made of cardboard or celluloid. Bank of America also launched their version of the credit card around this time.

1958 – Bank of America and American Express saw the overwhelming success of the Diners Club Card and wanted to get in on the action. America Express created a purple charge card for travel and entertainment expenses. In 1959, AMEX introduced the first card made of plastic because previous cards were made of cardboard or celluloid. Bank of America also launched their version of the credit card around this time.

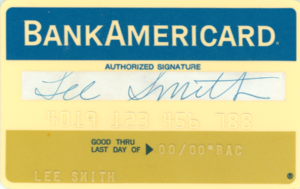

1966 – Bank of America introduced the first general credit card, similar to the credit cards we use today. Banking regulations back then limited the geographic reach of individual banks, so Bank of America found it difficult to compete with the Diners Club Card’s nationwide success. To overcome this restriction, Bank of America licensed their card to other banks. Initially, that move was successful, but they soon became overwhelmed with the administrative task of processing all of the paper slips from member banks. In an effort to address the growing needs, Bank of America decided to spin off the organization and it ultimately became known as Visa.

1966 – Bank of America introduced the first general credit card, similar to the credit cards we use today. Banking regulations back then limited the geographic reach of individual banks, so Bank of America found it difficult to compete with the Diners Club Card’s nationwide success. To overcome this restriction, Bank of America licensed their card to other banks. Initially, that move was successful, but they soon became overwhelmed with the administrative task of processing all of the paper slips from member banks. In an effort to address the growing needs, Bank of America decided to spin off the organization and it ultimately became known as Visa.

1986 – Sears, Roebuck & Company launched their first credit card, the Discover card. According to Discover, its first card was unveiled at the 1986 Super Bowl. Discover Card Services sought to create a new brand with its own merchant network, and the company has been successful at developing merchant acceptance. Discover credit card brought innovation, security, protection, and change to the credit card industry when it was first introduced.

1986 – Sears, Roebuck & Company launched their first credit card, the Discover card. According to Discover, its first card was unveiled at the 1986 Super Bowl. Discover Card Services sought to create a new brand with its own merchant network, and the company has been successful at developing merchant acceptance. Discover credit card brought innovation, security, protection, and change to the credit card industry when it was first introduced.

2004 – An anti-trust U.S. Supreme Court ruling against Visa and MasterCard changed the exclusive relationship that Visa and MasterCard enjoyed with banks. The court found that, rather than competing with each other, Visa and MasterCard had cooperated with each other by increasing their interchange fees. It allowed banks and other card issuers to provide customers with American Express or Discover cards, in addition to a Visa or MasterCard. People now have more choices than ever before.

2004 – An anti-trust U.S. Supreme Court ruling against Visa and MasterCard changed the exclusive relationship that Visa and MasterCard enjoyed with banks. The court found that, rather than competing with each other, Visa and MasterCard had cooperated with each other by increasing their interchange fees. It allowed banks and other card issuers to provide customers with American Express or Discover cards, in addition to a Visa or MasterCard. People now have more choices than ever before.

Conclusion –

Issuing credit cards is now a booming business. These lenders that issue cards to consumers make money through outstanding balance fees, annual fees, over-the-limit fees, and late payment fees to name a few. On the front end, when consumers make purchases with their credit cards, lenders make roughly 2% of the sales price.

The fees that lenders charge when credit cards are used for store or online purchases are known as an Interchange Fee. The lending industry has come under fire during the past few years because these interchange fees have risen 119% in the past five years. Interchange prices are fixed regardless of volume, which has displeased many larger retailers such as Amazon. Credit cards are now a fundamental part of our lives with roughly 72.1% of all American families having some type of credit card.

If you need help getting your credit card debt under control and get on the path towards becoming debt-free, give Advantage CCS a call today. Advantage Credit Counseling Service will help you resolve your debt problems and get you back on track. Unlike high-pressure debt relief companies, we will help educate you to make good financial decisions or recommend a custom debt solution. Headquartered in Pittsburgh since 1968, ACCS today is a nationwide, nonprofit credit counseling agency that has paved the road to financial freedom for nearly one million customers. Visit us at www.advantageccs.org